The French Competition Authority has issued a Statement of Objections involving various parties within the home appliance sector and where Electrolux France is alleged to have acted in breach of antitrust rules in France between 2009 and 2014.

A Statement of Objections is a formal step in an investigation whereby the investigation services of the French Competition Authority (Autorité de la Concurrence) inform the concerned parties of its preliminary findings (before the case is presented to the judging panel of the French Competition Authority). The Statement of Objections does not prejudge the final outcome of the case.

As previously disclosed in press releases and annual reports, the company became in 2013 the subject of an investigation by the French Competition Authority regarding possible violations of antitrust rules. The Authority has thereafter decided to conduct two separate investigations one of which was completed in December 2018. The Statement of Objections that now has been issued relates to the other investigation.the French Competition Authority’s Statement of Objections it is alleged that various parties within the home appliance sector have breached the antitrust rules. In particular, Electrolux France is alleged to have breached the antitrust rules by conducting resale price maintenance in the home appliance sector between 2009 and 2014 and by exchanging with other parties competitively sensitive information relating small appliances in France between 2009 and 2014.

The Statement of Objections is currently being carefully analyzed and Electrolux is preparing its defense. Nevertheless, given the alleged infringements and the nature of this investigation, it cannot be ruled out that the outcome could have a material impact on the Group’s financial result and cash flow. At this stage it is however not possible to evaluate the extent of such an impact.

This is information that AB Electrolux is obliged to make public pursuant to the EU Market Abuse Regulation. The information was submitted for publication

Category Archives: Financial

STATEMENT BY STANISLAS DE GRAMONT, CHIEF EXECUTIVE OFFICER OF GROUPE SEB:

2022, in a difficult general economic environment and after a record year in 2021, our sales were globally resilient. We are particularly pleased with our performance in China, where Supor for the first time exceeded the two-billion-euro turnover mark. However, our results were impacted by significant headwinds. In this context, the Group was once again able to demonstrate responsiveness and quickly implement effective action plans to adapt to market developments and protect its profitability.

At the same time, and beyond short-term imperatives, we have continued to invest in our strategic levers: product innovation, the international deployment of our champion products, the attractiveness of our brands, and the activation of all distribution channels. No truce either for our investments in our competitiveness – industrial, logistics, information systems -, which are all crucial for the future. I would like to salute and thank the unfailing commitment of all the teams, which has been essential in these achievements.

For the year 2023, visibility remains limited. Despite a first quarter that is anticipated to be down, the Group expects a gradual improvement in sales in its Consumer business, strong revenue growth in Professional sales, as well as an increase in its operating margin for the year as a whole.

We are confident in the continued development of the global market for Small Domestic Equipment and Professional Coffee, in which we continue to strengthen our presence with the recent acquisition of the La San Marco company. We remain convinced of the relevance of our economic model, which will allow us to take full advantage of strong structural demand, a source of growth opportunities for Groupe SEB.

Electrolux rumours

There have been rumors about the sale of the Swedish company for some time now

“we don’t comment on rumors,” Electrolux PR manager Paul Palmstedt told the Swedish financial publication Privata Affaerer .

Chinese company Midea had been rumoured to be interested

Electrolux is not sailing in good waters at the moment. It loses on the North American market and does not gain on the European one which is suffering from weak demand. Things are going better in the professional segment and partly in the built-in segment, sure, but the cost base is high and making margins isn’t easy.Midea has repeatedly stated that it sees its future in high value-added productions such as advanced robotics and automotive. It is said that you intend to invest money and intellectual resources in a business like ‘white’ which will be stagnant in the next few years at best.Electrolux collaborates with Midea in China to promote AEG without the need to exchange shares. One can think of a partial entry of Midea into the shareholding structure of Electrolux, or of joint ventures for the marketing in Europe (and in the USA) of products made by Midea but conceived and sold by Electrolux.

MediaWorld: turnover of 2.7 billion euros in fiscal year 2022 (+2.4%)

Mediaworld announces that it achieved a turnover of 2.7 billion euros (+2.4% compared to the previous year), one of the highest in the thirty-year history of the company and the best of the last ten years . Ebit stood at 26.6 million euros, up by 3.2 million (+13.7%) compared to the 2019 fiscal year (last pre-pandemic). The brand’s 2022 financial year is part of a macroeconomic framework strongly conditioned by various economic factors that have had an impact on the business: from the intensity of the war in Ukraine to the increase in the inflation rate (+8.9% on annual basis in September 2022) following the increase in the cost of energy. Furthermore, the consumer electronics market also recorded a slight contraction (-1.9% in September 2022).

Among the key factors that affected the positive performance of sales, an official note reads, the implementation of a substantial investment plan aimed at upgrading the technological infrastructures and strengthening the stores, with new openings, contributed significantly and renovations of the shops already present in the area. In particular, in 2022 MediaWorld allocated 40.2 million euros to investments, 140% more than the previous year; of these 28.5 million euros were invested for the complete renovation of 22 points of sale, the opening of 3 new stores and the second Tech Village in Rome. Approximately €11.7 million has been earmarked for IT infrastructure improvements including the implementation of the new website launched in July 2022,

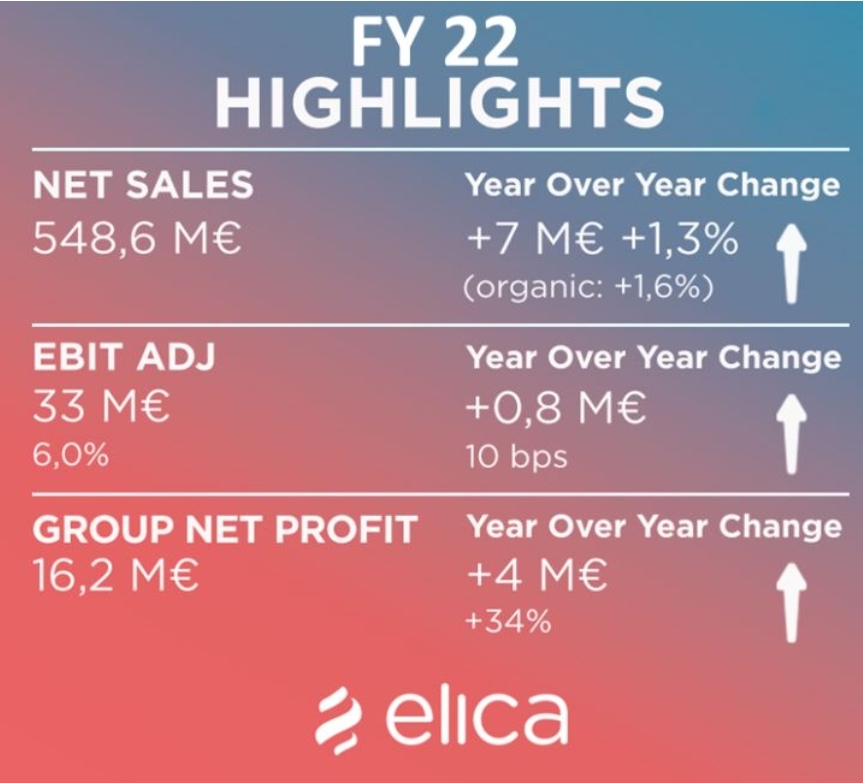

Elica record sale’s

Elica BoD approves the preliminary FY 2022 results.

Second Record Year in a row in terms of sales, EBIT margin, and net profit, despite the most adverse inflationary, demand, and geopolitical scenario of the last decades.

The company was able to improve margins versus last year, despite ~60 million of cost inflation, thanks to the business model flexibility and the agile execution of our turnaround projects.

Looking forward to 2023, it will be an even more challenging year, but we have a clear strategy for both the Cooking and Motor Divisions in terms of products, customers, and regional distribution.

Groupe Seb soars on the Stock Exchange

With a leap of 7%, the Paris Stock Exchange greeted Groupe SEB’s financial statements yesterday. Sales (7.96 billion) are only 1.2% lower than those of the record year 2021 and up 8.2% on 2019. The fourth quarter closed with revenues down by 3, 6% to 2.4 billion. In both cases the trend is higher than analysts’ expectations, as reported by Radioco.

The Seb group owns 32 brands, including Tefal, Seb, Rowenta, Moulinex, Krups, Lagostina, Wmf, Emsa and Supor. It is present in 150 countries and has over 33,000 employees.

After a record 2021, Seb group sales delivered a resilient performance in 2022. The group’s business held up well in most of the geographic areas in which it operates and the fourth quarter marked a slightly more favorable trend’” , commented the CEO Stanislas de Gramont , recalling that“from the second quarter the ‘Consumer’ activity (-2.6% to 7.2 billion) is influenced by the impact of the war in Ukraine and by issues specific to some markets’, in particular France (-22%) and Germany (-13%), ‘but it recorded a satisfactory performance in other countries, including China’. The ‘Professional’ hub (+15.6% to 725 million) recorded ‘a strong dynamic throughout the year and continues to be an important growth lever for the entire group ‘. Seb ‘confirms the operating margin target for 2022 and estimates that it will be in the high end of the range between 7% and 7.5%’.

Electrolux results

Highlights of the full-year of 2022

In full-year 2022, net sales were SEK 134,880m (125,631) and operating income excl. non-recurring items was SEK 831m (7,528). Earnings declined due to lower volumes, as a result of weaker market demand, and to elevated cost levels from production inefficiencies in North America. Strong price execution and attractive product and brand offering contributed positively to earnings.

Highlights of the fourth quarter of 2022

In the fourth quarter, net sales amounted to SEK 35,769m (35,372) and operating income to SEK -1,964m (882), corresponding to a margin of -5.5% (2.5).

Operating income includes non-recurring items of SEK -1,352m (-727). Excluding these non-recurring items, operating income amounted to SEK -612m (1,609), corresponding to a margin of -1.7% (4.5). The year-over-year decline was a result of lower volumes in all four business areas and significantly higher cost levels in Business Area North America, which reported an underlying loss of SEK 1.2bn.

Income for the period amounted to SEK -1,922m (596) and earnings per share were SEK -7.12 (2.09).

Operating cash flow after investments was SEK 242m (2,103).

The Board of Directors proposes that no payment of dividend will be made for 2022.

Decision on February 1, 2023, to discontinue production at the Nyíregyháza factory in Hungary from the beginning of 2024 will result in a negative non-recurring item of approximately SEK 550m in the first quarter of 2023.

President and CEO Jonas Samuelson’s comment

In 2022, new challenges presented themselves in addition to supply chain constraints: high general inflation, raised interest rates, soaring energy prices, and increased geopolitical tensions. These negatively impacted consumer demand for household appliances, especially evident in the latter part of the year.

In the fourth quarter, significantly lower sales volumes resulted in an organic sales decline of 8.4%. The volume decline across all regions was coupled with severely elevated cost levels in our North American operation. This resulted in an operating loss for the Group of SEK 612m, excluding non-recurring items. We have firm plans in place to structurally lower costs under the Group-wide cost reduction and North America turnaround program and in the quarter we continued to reduce discretionary spending. A strong focus on inventory management and adjusting production rates to the current demand environment resulted in an overall inventory reduction from previously high levels, especially of in-house produced finished products that at the end of the year were at overall normal levels.

On a positive note, I am pleased with how well received our product launches across all regions have been during 2022. This was particularly evident in the fourth quarter with the strong earnings contribution from our attractive product offering, even in this challenging demand environment with reduced consumer purchasing power. This strengthens my confidence in our ability to drive mix improvement also going forward, with an average consumer star rating of 4.64 for the Group in 2022. Another achievement was the strong net price realization across all regions, despite promotional activity returning to normal levels towards the end of 2022. I am very pleased that we through price increases fully offset significant cost inflation, primarily in raw material and logistics, both in the full-year as well as in the quarter.

It is encouraging that we have reduced our climate footprint significantly and already in 2022 reached the 2025 science-based climate target to reduce CO2 emissions in our own operations by 80% compared to 2015. We are now reviewing our targets going forward, raising the bar on our own sustainability agenda even further.

Based on our review of production capacity needs, we have decided to discontinue production at the Nyíregyháza factory in Hungary from the beginning of 2024. The strategic direction is to optimize the refrigeration production footprint from a cost perspective through both outsourcing and own production leveraging Group scale.

Looking into 2023, consumer sentiment is anticipated to continue to be negatively impacted by a high inflation and interest rate environment, although with regional differences. Demand for core appliances in 2023 full-year is therefore expected to be negative for all regions except for the Asia-Pacific, Middle East and Africa region, which is assessed to be flat compared to 2022.

On the back of this, we estimate our volumes in 2023 to decline year-over-year, partly mitigated by mix improvements from our strong offering. We expect External factors to be negative for the year, driven by energy and labor cost inflation as well as currency headwind and most of this will impact Europe and Latin America. Although we foresee benefits from lower raw material costs, the positive impact on earnings is reduced as a higher share than normal of raw material procured at last year’s rates will be consumed in 2023. This as a consequence of higher inventory levels of supplies and reduced production rate in the fourth quarter of 2022. Given the regional variations in cost inflation and demand outlook, we anticipate differences in the price dynamic for our business areas, with high promotional activity in North America. Hence, we see a challenge to fully offset an anticipated negative impact from External factors in 2023 full-year with price on a Group level. The expected positive year-over-year earnings contribution of SEK 4-5bn from Cost efficiency and reduced investments in innovation and marketing combined, related to the Group-wide cost reduction and North America turnaround program, is reconfirmed.

I am convinced that we have the right strategy as well as the experience and the organizational structure needed to navigate in volatile environment and seize opportunities. A successful implementation of the Group-wide cost reduction and North America turnaround program will be our number one priority for 2023.

Whirlpool: disappointing data

Whirlpool Corporation reported data from a disappointing fourth quarter during which sales fell 15.3% from 5.8 to 4.9 billion (-15%) with a loss of 1.6 billion due to weak demand only partially offset by a more favorable price mix (demand was directed towards higher-end products) and by the increase in prices

Full-year 2022 sales fell 10.3% from $22 billion to $19.7 billion, a loss of $1.52 billion versus a profit of $1.8 billion in 2021, or nearly $7 per share .

In Emea the turnover collapses but without losses.

Sales in EMEA fell by 27% from $1.4 billion to $1.0 billion (also depressed by the fall in the euro against the greenback: in local currencies the decline was 18%) with a small loss however 4 million dollars.It was unclear whether Whirlpool expects any cash proceeds from the transaction that transferred Whirlpool’s EMEA operations to Beko Europe

Electrolux to discontinue production at Nyíregyháza factory in Hungary

Electrolux has decided to discontinue production at the Nyíregyháza factory in Hungary from the beginning of 2024. The company will take a restructuring charge of approximately SEK 550 million which will be reported as a non-recurring item affecting operating income for Business Area Europe in the first quarter of 2023.

The decision follows a review of production capacity needs including an investigation into the competitiveness of the Nyíregyháza factory, which employs around 650 people and manufactures refrigeration products. The strategic direction is to optimize the refrigeration production footprint from a cost perspective through both outsourcing and own-production leveraging Group scale.

The decision means that remaining investments in refrigeration products that are part of the earlier communicated global re-engineering investments of SEK 8 billion, which started in 2018, will be revised and redirected in line with the strategic direction of Electrolux.

Electrolux is exploring possibilities to divest the factory in Nyíregyháza and is committed to collaborating with relevant authorities and stakeholders to support its employees in the best possible way during this phase.

The cash flow impact is estimated to be approximately SEK 300 million, mainly in 2024-2025. The final operating income and cash flow effects will be determined by the exchange rate on the relevant recording dates.

Appliances become trillion euro market

Appliances market size will grow reach over a trillion euros ($1.096 trillion) by the year 2030, according to a study by Precedence Research. But what are the key drivers for this market growth in the years to come?

A number of Technological advancements have been identified in the study as key reasons why the global household appliances market is expected to grow so much in the next seven years. Precedence Research cites the proliferation of digital technologies, as well as heightened investment from industry leaders in developing innovative appliances and services, as drivers for market growth.

New technologies emerging in the household appliance industry, such as robotics, artificial intelligence, machine learning and the internet of things, were listed as more causes for the market growing to over a trillion euros by 2030.

Developments within e-commerce, predicted to be the fastest-growing segment for household appliances, were also cited as drivers for market growth. E-commerce channels are seen to be enjoying an increase in sales of household appliances, due to the growing influence of e-commerce platforms, as well as wider availability of smartphones and the internet.

Refrigerators were noted as being the most in-demand household appliance, as well as the main driver of growth in terms of market segments. The report suggests that in the coming years, demand for refrigerators will partly be driven by the availability of different types of product, based on size, door and additional functions.

Precedence Research states that the Asia Pacific region is the most dominant in terms of household appliance revenue, with the area being the base for industry leaders such as LG, Panasonic and Samsun